The Order Management Software Market – 2023

PRODUCT OVERVIEW

In this report we look at how retailers are investing in one enterprise order management system (OMS) and the in order to stay competitive.

Summary:

Retailers are racing to compete with Amazon and Walmart. And retail supply chain disruptions, record inflation and a looming global recession are greatly challenging retailers after multiple years of growth. Companies must get to a single version of the truth on customers so that they can be profitable in all channels. They must turn their stores into a competitive advantage and they must be able to fulfill orders from anywhere. To do so they are investing in one Enterprise Order Management system. In fact, the Enterprise Order Management Software system is the core for retail going forward. Having that single order management system that allows for shipping from the warehouse, pickup at store, or simply traditional store fulfillment is key to not only surviving but thriving in the future.

This study reviews the trends and barriers around reaching this goal of a single order management system, the painful process of removing silos, and the goal of using stores and their locations as their competitive advantage. This research looks at the top vendors in this area, the size of the market and the positioning of those vendors. It is designed for retailers and vendors that are looking to move to the central order management process.

HIGHLIGHTS

One of the most exciting developments that retailers are currently embracing is Unified Commerce. We define Unified Commerce as the holistic technology stack that provides one version of the truth for data pertaining to customers, products, pricing and sourcing, that in turn enables the procurement, sale and delivery of merchandise independent of channel. Those solutions that fit within the Unified Commerce umbrella are showing extremely healthy adoption moving forward across a broad range of retail segments and tiers. In retailer discussions the main reasons given include cost savings and a more seamless data flow (for both the retailer and the consumer).

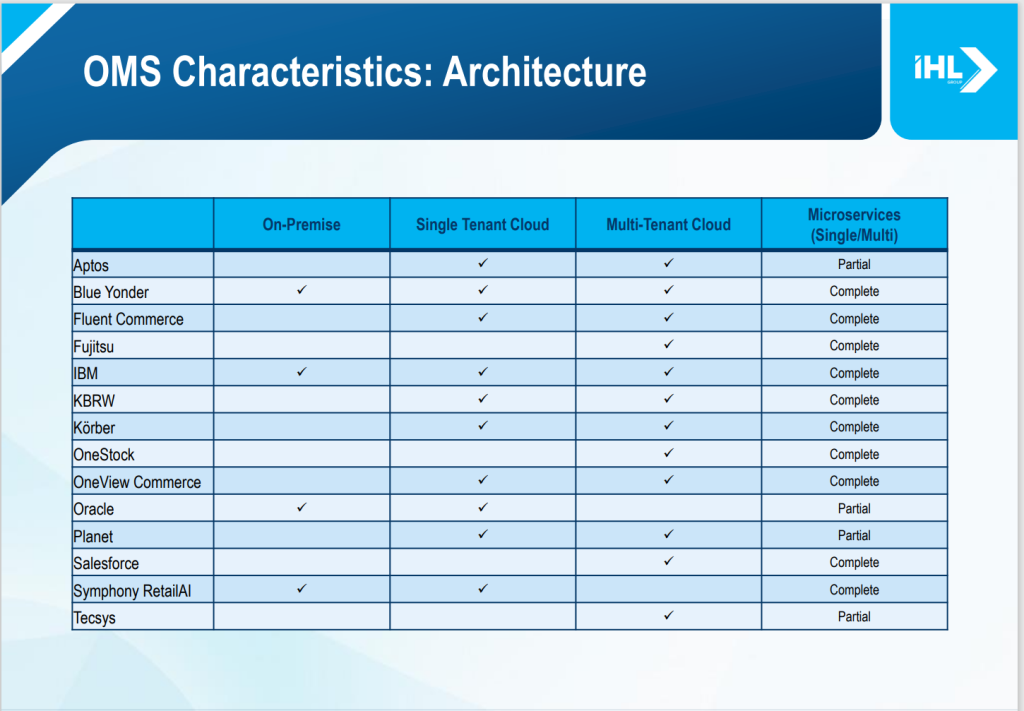

The most successful retailers had embraced the concept of Unified Commerce wholeheartedly before the COVID pandemic and enjoyed the benefits once consumers moved quickly to multichannel shopping. The foundation for a successful Unified Commerce strategy is a highly capable and configurable enterprise order management system (EOM) that is able to look at orders independent of the originating order channel. EOM with be linked with the five key technology pillars consisting of Store/POS, E-Commerce, Sales/Marketing/CRM, Merchandising/SCM and BI/Analytics, resulting in the figure shown to the right. OMS will be the natural extension of key Point-of-Sale (POS) functionality such as enterprise inventory visibility, ordering from other stores, return of online purchases, ship from store, order online from the POS, click and collect, and store to store transfer. The broad functionality required by OMS is extended even further when one considers the additional permutations for ordering and return brought by online and phone/catalog sales.

Below is the TOC for the research.

Table of Contents

1.0 Introduction and Key Definitions

2.0 Retail OMS Market Overview

3.0 Trends, Drivers and Barriers

4.0 Vendor Positioning Maps

5.0 Leading OMS Vendors & Differentiators

6.0 Vendor Profiles

7.0 Methodology

FAQS

Is this a comprehensive view of the marketplace?

Yes, this provides a view of the market by size worldwide. We do breakouts on sizing also specifically for the North America and EMEA markets.

People use different terms – Enterprise Order Management, Distributed Order Management?

We don’t delineate in this report. Really, any order management system of the future needs to be able to distribute orders depending on the channel and best way to fulfill. To us it is just semantics.

Can I share this study in my company?

Yes if you have an enterprise license. See below for more.

Can I share this study with partners and clients?

Not in entirety unless you have negotiated a distribution license with IHL. Basically we don’t want the study going to partners and clients who should otherwise purchase a license. This is what we do for a living, and if people violate this we can no longer do the research. Contact us at ihl(at)ihlservices.com with any questions.

Can I quote this study in my presentations and press releases?

In most cases this is fine but we ask that you run it by us first at ihl(at)ihlservices.com. Typically things shared in percentages (ie. this is 20% increase) then that is fine. Items in raw $$$ or units typically we will not allow to share. But we can work with you on this. We realize that you buy the research to use, so we can usually find a nice compromise that protects our IP and meets your needs.

Can I get access to the analysts who wrote or partnered in the study?

Yes, one of the core differentiators of IHL Research Studies is that included in part of the price is up to 1 hour with the analyst to ask follow-up questions or dig further into any assumptions. This does not extend to getting more data, just better insight into how we arrived at the data and came to the conclusions from that data.

PRICING

License Options

Enterprise License – a license that allows for the research to be accessed and shared internally with anyone else within the organization and wholly owned subsidiaries.

Distributable License – a license that allows the purchasing company to distribute the report to clients and potential clients and investors.

For detailed license policy for non-distribution licenses, click here. For summary, see below.

IHL Group License and Fair Use Agreement

All of IHL Group’s generally available research are electronic licenses and are limited by the license type chosen for purchase. For Single User Licenses this means that the person buying the research is the only person to use the research.

For Enterprise Licenses, these can be shared freely within the company. We only ask that this information not be shared with partners or others outside the purchasing company without authorization from IHL Group. The license does not extend to joint ventures or other partnerships. If the relationship is not a wholly-owned subsidiary, then both parties would need a license.

For Distribution Licenses, the purchasing company can freely share the content with partners, customers and potential investors. They cannot resell the content but can use fully for presentations and/or derivatives as part of this license.

Practically, this implies the following:

- The purchasing company can use the data and research worldwide internally as long as the international organizations are wholly owned subsidiaries of the purchasing company.

- The data or any research cannot be distributed in whole or in part to partners or customers without express written approval from IHL Group.

- The purchasing company may quote components of the data (limited use) in presentations to customers such as specific charts. This is limited to percentage components, not individual unit information. Unit data cannot be shared externally without express written approval from IHL Group. All references to the data in presentations should include credit to IHL Group for the data.

- The purchasing company can reference qualitative quotes in printed material with written approval from IHL Group.

- All requests requiring written approval should be submitted to ihl(at)ihlservices.com and will be reviewed within one business day.

Distribution License – a license that allows for sharing content and derivatives outside of the purchasing company.

For Distributed Licenses, if applicable, the research can be shared with prospective customers, investors. It cannot be shared with partners or other technology vendors who should be purchasing their own licenses.

For any questions regarding this policy, please contact us at 1-888-IHL-6777 (North America) +1.615.591.2955 (International) or email us at ihl(at)ihlservices.com.