How Retail Leaders Outperform – What We Learned from 400+ Brands

Product Overview

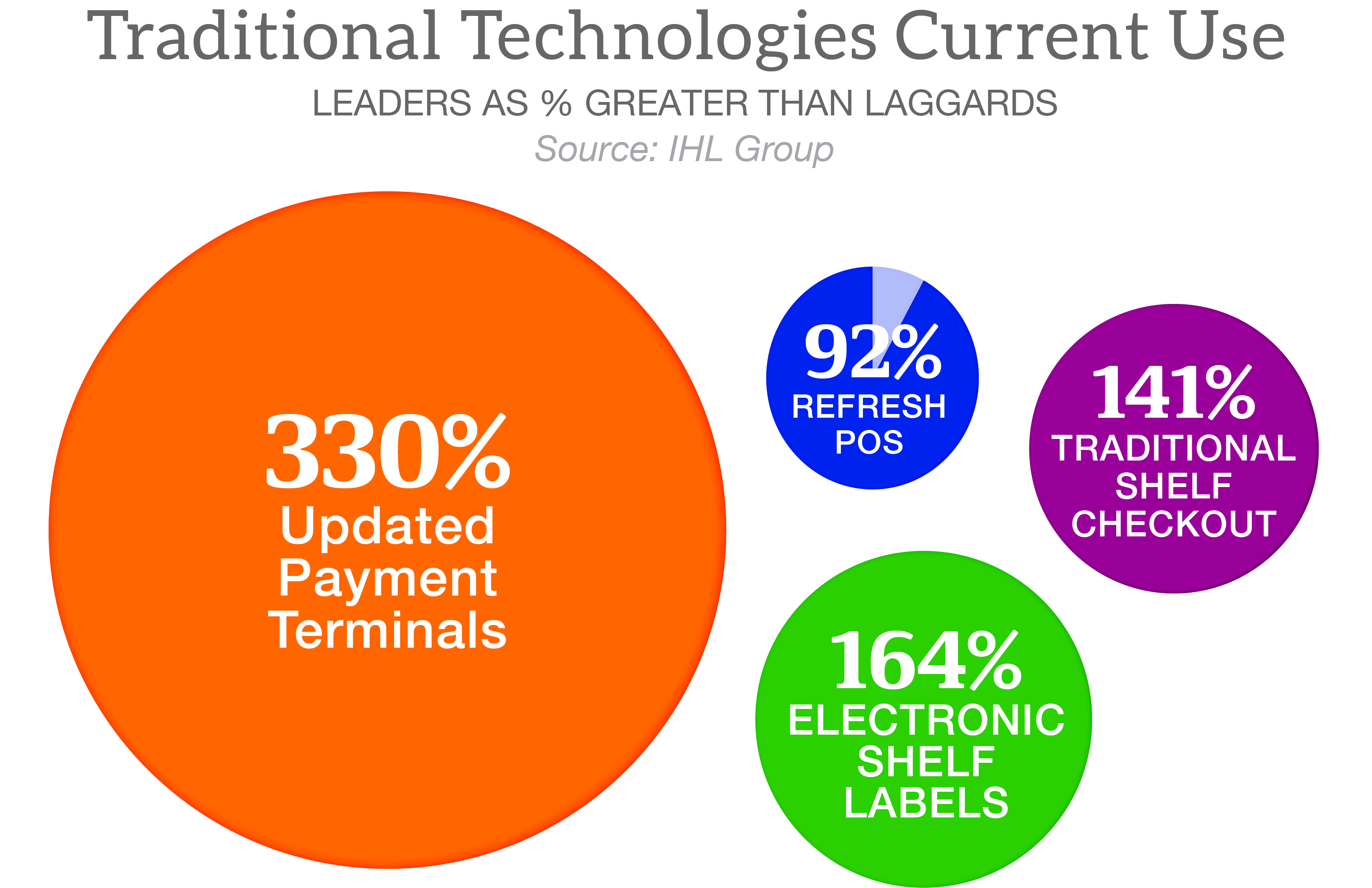

How Retail Leaders Outperform

Move beyond the hype. We identify the specific technologies measured by performance and spend that distinguish retail winners from laggards. This study of over 400+ retail brands covers 33 different technologies and 12 top tech priorities for 2026.

See where the market is going, not where it has been. This is our keynote study of the year. Along with the analyis, those who purchase get up to 125 key data items that you can use to create social posts.

Retailers acting as early adopters see profit margin gaps nearly double that of competitors who wait for clear ROI evidence.

While others remain in pilot phase, leaders move the needle with RFID-enabled checkout and 100% inventory accuracy.

ESLs drive operational agility, allowing leaders to pivot pricing and promotions in real-time across the enterprise.

Reality Over Hype

We cross-reference tech installs with financial performance to find signal in the noise. We track where actual checks are being written.

Measured Technologies

- Modernized POS/mPOS

- Electronic Shelf Labels

- RFID (Checkout/Inv)

- Edge & Microservices

- Computer Vision/CV

- 5G & Geo-Location

- Headless Commerce

- Robotics & Smart Shelves

The #2 overall priority. Leaders prioritize this 208% higher than laggards.

Moving from pilots to production by cleaning and training proprietary data sets.

Optimizing BOPIS and Ship-from-Store to reclaim digital journey profitability.

“Grounding Facts for Retail Strategy”

“IHL data provides grounding facts for our solutioning and GTM strategy. Their focus on inventory distortion has driven our entire strategy for a decade.”

“IHL commands respect from operators and experts alike. They provide trends and analysis that retail executives depend upon.”

HIGHLIGHTS

Key Highlights

Along with research study analysis your license also includes the raw data in spreadsheet form to do your own cross tabs. You can cross tab any answer to any other answer for unique insight.

We break down the data to find answers to questions that many in our industry are asking, like the following:

- What do the IT Spend, Store Growth and Store Remodels look like for 2025?

- How does AI impact technologies?

- What are the retailers’ Top System Priorities?

- What does 2026 look like for POS, Software, Emerging Technologies? What are the trends driving change?

- How fast is Edge Computing, RFID, Computer vision or Microservices growing?

- What digital customer journeys are profitable for retailers and which are optimized? What is the value of optimizing these journeys.

- Which segments are looking to replace POS clients or POS Software? Will it be a good year for Contactless Payments?

- Who is planning to deploy which Mobile Platforms, and when?

Table of Contents

- Executive Summary

- Financial Performance

- Customer Journeys

- Technology Adoption Types

- Tech Priorities for 2026

- Traditional Technologies

- Checkout Solutions

- Other Traditional Technologies

- Windows 10 Sunset Strategies

- New Initiatives

- Leaders / Laggards

- Early Adopters Advance

- Labor Expectations with AI Impact

- What About Tariffs – How are Retailers Reacting

- Which Technologies Really Move The Needle?

- Strategic Recommendations For Retailers In Our Study

- AI Impact – Major Impacts in Sales Improvements and Expectations

- Appendix and Methodology

PREVIEW

Click on a thumbnail to expand.

FAQS

Is this a comprehensive view of the marketplace?

No, this is a survey of more than 400 brands with stores in all retail segments and their purchase intentions. While a full market overview would include everyone, this is just the answers of those that responded to the survey. Caution should be used in extrapolating these results to the entire market. For some comprehensive market research on store automation technologies, you should Click Here.

Did this survey cover larger or smaller retailers?

Actually both. Roughly 45% of the respondents were retailers over $1 Billion. Another 10% were retailers over $500 Million but less than $1 Billion. The remaining retailers were under $500 Million in annual sales. The data is broken down by retailer size so you can see the differences.

Can I share this study in my company?

Yes if you have an enterprise license. See below for more.

Can I share this study with partners and clients?

Not in entirety unless you have negotiated a distribution license with IHL. Basically we don’t want the study going to partners and clients who should otherwise purchase a license. This is what we do for a living, and if people violate this we can no longer do the research. Contact us at ihl(at)ihlservices.com with any questions.

Can I quote this study in my presentations and press releases?

This is fine in most cases, but we ask that you run it by us first at ihl(at)ihlservices.com. Typically sharing percentages (ie. this is a 20% increase) is fine, but sharing raw $$$ or units is not. We realize that you buy the research to use, so we can usually find a nice compromise that meets your needs while protecting our IP. We can work with you.

Can I get access to the analysts who wrote or partnered in the study?

Yes, one of the core differentiators of IHL Research Studies is that included in part of the price is up to 1 hour with the analyst to ask follow-up questions or dig further into any assumptions. This does not extend to getting more data, just better insight into how we arrived at the data and came to the conclusions from that data.

PRICING

License Options

Enterprise License – a license that allows for the research to be accessed and shared internally with anyone else within the organization and wholly owned subsidiaries.

IHL Group License and Fair Use Agreement

All of IHL Group’s generally available research are electronic licenses and are limited by the license type chosen for purchase. For Single User Licenses this means that the person buying the research is the only person to use the research.

For Enterprise Licenses, these can be shared freely within the company. We only ask that this information not be shared with partners or others outside the purchasing company without authorization from IHL Group. The license does not extend to joint ventures or other partnerships. If the relationship is not a wholly-owned subsidiary, then both parties would need a license.

Practically, this implies the following:

- The purchasing company can use the data and research worldwide internally as long as the international organizations are wholly owned subsidiaries of the purchasing company.

- The data or any research cannot be distributed in whole or in part to partners or customers without express written approval from IHL Group.

- The purchasing company may quote components of the data (limited use) in presentations to customers such as specific charts. This is limited to percentage components, not individual unit information. Unit data cannot be shared externally without express written approval from IHL Group. All references to the data in presentations should include credit to IHL Group for the data.

- The purchasing company can reference qualitative quotes in printed material with written approval from IHL Group.

- All requests requiring written approval should be submitted to ihl(at)ihlservices.com and will be reviewed within one business day.

For Distributed Licenses, if applicable, the research can be shared with prospective customers and potential institutional investors. It cannot be shared with partners or other vendors who should be purchasing their own licenses.

For any questions regarding this policy, please contact us at 1-888-IHL-6777 (North America) +1.615.591.2955 (International) or email us at ihl(at)ihlservices.com.